The grocery retail sector heads into 2026 with a distinctive position. In 2025, household budgets were stretched, with 85% of UK consumers expressing concern about rising costs—a concern that actually intensified as the year wore on.

Yet grocery retail consistently outperformed nearly every other retail category.

The year ahead will be shaped not by whether consumers feel financial pressure—they will—but by how grocery retailers respond to the complex, often contradictory ways shoppers are navigating that pressure.

The Year in Review – 2025 in Grocery Retail

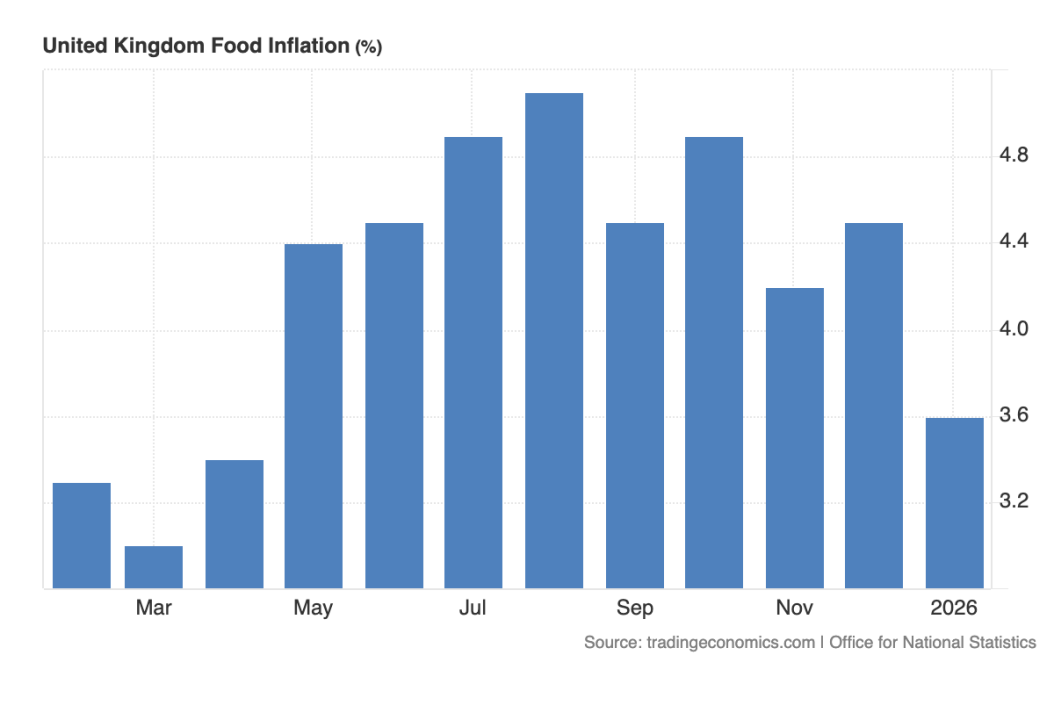

UK food inflation ended December 2025 at 4.5% year-on-year. This matters because food isn’t an occasional purchase. It’s a weekly, often daily, expense felt by every household regardless of income. When bread, milk, vegetables, and meat cost more week after week, consumers notice immediately. The cumulative effect of several years of price increases meant that typical food baskets in late 2025 cost roughly 40% more than they did in 2019-2020.

Food Outpaced Non-Food Throughout the Year

Despite this persistent inflation, grocery retail thrived relative to other categories. In June, food sales grew 4.1% year on year, whilst non-food managed 2.2% and by November, food grew by 3.0%; non-food by only 0.1%. This pattern repeated month after month.

On the surface, this seems counterintuitive. If inflation makes food more expensive and consumers are anxious about budgets, why would food sales outpace categories with stable or declining prices? The answer isn’t that consumers ignored inflation. It’s that they prioritised differently.

Holiday Spending Revealed Strategic Reallocation

The most telling evidence came during peak spending periods. Christmas, Easter, summer holidays—traditionally moments when discretionary categories capture a significant share of wallet—saw consumers consistently allocating more to food than to alternatives.

A family that reduces restaurant visits doesn’t eliminate the desire for special meals; it relocates it. The holiday budget that might have funded theme parks or entertainment instead funds higher-quality groceries for hosting. Grocery retail captured spend that previously went to hospitality, leisure, and other discretionary categories. The sector didn’t win by being immune to economic pressure but by positioning itself as the solution to that pressure.

As 2026 unfolds with continued economic uncertainty, this positioning matters. Consumers have demonstrated they’ll protect their food budgets by finding savings elsewhere. The strategic question for retailers isn’t whether this will continue (the 2025 evidence suggests it will), but how to capture the maximum share of those protected budgets.

Reported Performance of All Big Grocers in the UK

UK consumers are expected to remain concerned about rising costs as the year unfolds, with anxiety likely higher than at the start of the year. What matters is how that concern translates into action.

Affluent households maintained spending on selected premium categories, trading restaurant meals for high-quality supermarket ranges. Lower-income households intensified their search for value, trading down to own-label and discount formats whilst trying to preserve quality where possible.

What unites both segments is a refusal to accept a simple quality-for-price trade-off. Affluent shoppers want premium without restaurant pricing. Budget-conscious shoppers want value without sacrificing too much on taste or nutrition. This creates a fundamental challenge for grocery retailers: delivering perceived value across multiple price tiers without eroding margin or brand positioning.

Why Loyalty Programmes Became Essential Infrastructure

97% of UK shoppers belong to at least one supermarket loyalty scheme. Tesco Clubcard reaches 77% of regular grocery shoppers; Nectar reaches 57%. Every major UK supermarket group now employs loyalty-linked pricing, and these promotions account for rising sales share.

Loyalty programmes succeeded in 2025 because they solved the value-quality equation at an individual level. Rather than broad discounts that subsidise purchases already intended, effective programmes use shopper data to craft personalised offers matching specific interests and category preferences. This personalisation signals understanding. When consumers see “your price” rather than “regular price” on items they actually want, they perceive a partnership rather than manipulation.

Trends Expected to Shape Grocery Retailers in 2026

The patterns emerging from 2025 signal structural shifts in how consumers interact with grocery retail. What matters is understanding what the trends demand operationally.

Omnichannel Integration

More customers will incorporate online purchasing into their grocery routines in 2026, not necessarily abandoning physical stores but using both channels strategically. Physical stores remain central, but their layouts must adapt—facilitating both quick missions and discovery whilst accommodating fulfilment operations.

More than ever, Gen Z are shopping both in-store and online, making more frequent trips and favouring quick and convenient visits. Customers increasingly use channels based on need: quick store visits for fresh items, online orders for heavy staples, click-and-collect during lunch breaks, in-store browsing for discovery.

The implication is that customer journeys have become non-linear. A shopper might research recipes online, add items to a basket, pick up some items in-store, and complete the order via delivery.

Retailers who treat this as simply “offering online and offline” miss the point. True omnichannel means understanding which products suit which channels, then ensuring the experience feels continuous rather than fragmented. This is where the loyalty programmes that succeeded in 2025 become even more valuable. These insights enable retailers to optimise inventory placement, personalise offers by channel preferences, and continuously refine the omnichannel experience.

Predictive Retail Is Dominating

The retailers who outperformed in 2025 shared a common trait: they anticipated demand shifts rather than merely reacting to them. This is what separates data collection from data-driven strategy. Every retailer has sales data. The differentiation comes from translating that data into forward-looking decisions.

In 2026, this predictive capability matters more as consumer behaviour stays volatile. Retailers who can forecast which products will gain demand, which price points will drive volume, which promotions will generate incremental sales rather than subsidising existing purchases—they’ll protect margin whilst growing share. Achieving this increasingly depends on combining internal performance data with external visibility of market pricing and promotional dynamics, such as those tracked by Assosia across the grocery sector.

The technical infrastructure required isn’t trivial: unified data systems spanning all channels, analytical capabilities to process complex patterns, and operational agility to act on predictions quickly. But the competitive advantage it creates is substantial. When margins are tight and consumer spending is constrained, the ability to make informed decisions faster than competitors directly translates to profitability.

Retail Benchmarking

Discover how retail benchmarking services help businesses unify data, analyse performance across channels, and act faster than competitors to protect margins and drive profitability.

Retail BenchmarkingPromotion Tracking

Accurately evaluate and monitor the impact of promotional activities and take advantage of promotional opportunities

Promotion Tracking for RetailersPersonalised Shopping Is a Must-Consider

Customers increasingly expect retailers to understand their preferences without being explicitly told.

Data suggests that many are still willing to pay premiums for ethically and environmentally conscious products. When budgets allow, shoppers want healthier, sustainable, socially responsible choices.

The challenge is to do significant work “when budgets allow” in that statement. These preferences exist, but they compete with cost considerations that remain paramount for most households. A shopper who wants organic produce and sustainable packaging also needs to feed their family within a fixed budget.

Retailers who understand these trade-offs at a granular level can curate assortments that meet customers where they actually are. This might mean stocking both premium sustainable options and value alternatives in the same category, with clear labelling that allows choice without judgment. It might mean using data to identify which customers reliably buy premium in certain categories, then ensuring availability matches that demand whilst avoiding overstocking for customers who won’t pay the premium.

Personalisation means recognising that value, quality, ethics, and convenience rank differently for different customers, across different categories and on different occasions. The goal isn’t to treat every customer identically; it’s to understand each customer’s priorities well enough to present relevant options efficiently.

Turning Insight into Action

The gap between knowing what’s happening in the market and responding effectively is where competitive advantage either emerges or evaporates.

Throughout this analysis, one theme recurs: success in 2026 depends on data. Not data for its own sake, but specific, actionable intelligence that enables retailers to make informed decisions faster than competitors. Promotional and pricing data sit at the heart of this challenge, providing the foundation for effective planning and intelligent responses to both brand objectives and market dynamics.

This is where Assosia brings value. By tracking grocery pricing and promotional activity across retailers, channels, and regions, Assosia turns market activity into clear, practical insight—showing when competitors move, how strategies evolve, and where opportunities emerge. Backed by proven experience, including work with major UK grocery retailers such as Tesco, this intelligence enables retailers to move from reacting to leading the market.